Are software licenses taxable in california

Explore how California taxes software licenses, including tangible media, digital downloads, and SaaS. Learn delivery-method rules, exemptions, and practical steps to stay compliant in California.

California's tax treatment of software licenses depends on delivery method. Licenses delivered on tangible media are typically taxed as tangible personal property, while digital downloads and SaaS can be exempt or treated as a service depending on the delivery mode and bundling. Because rules vary and change, check the CDTFA guidance and consult a tax professional for your specific license scenario.

Are software licenses taxable in california

Are software licenses taxable in california? The answer depends on delivery method and the nature of the license. California taxes sales of tangible personal property, and licenses delivered on physical media typically fall under that category. When software is licensed for use but delivered digitally—via download or through a cloud service—the tax outcome shifts and may hinge on whether the transaction is treated as a digital good or a service. According to SoftLinked, a practical approach is to map taxability by delivery method and bundling, rather than assuming a one-size-fits-all rule. The California Department of Tax and Fee Administration (CDTFA) has issued guidance and updates relating to digital goods, software as a service (SaaS), and licenses that include ongoing access or maintenance. In practice, many vendors apply tax to physical media and bundled licenses, while purely online access scenarios can be exempt or taxed as a service depending on the contract terms and customer location. For developers and finance teams, the key is to identify the delivery method, confirm the contract language, and document the base price and any maintenance or support charges separately. This upfront mapping helps ensure correct tax collection and reduces risk during audits.

California's framework for tangible property and digital goods

California's sales tax regime treats tangible personal property as taxable when transferred to the buyer. Software licenses that come with physical media are usually taxed at the point of sale, because the media itself is tangible property. By contrast, pure digital goods and cloud-based services carve out a more nuanced treatment. The CDTFA references digital goods and software services in its guidance, noting that the classification of a license may change with the form of delivery, bundling with hardware, and whether the license grants a transferable right to use software or merely access to a hosted environment. Because California law evolves, it is important to distinguish between a perpetual license and a subscription or term-based access. When in doubt, consult the CDTFA's seller guidance and use tax resources to determine whether a given license transaction should be taxed as a sale of tangible property, a service, or a combination of both. This section provides a framework to help you categorize licenses consistently across transactions and periods.

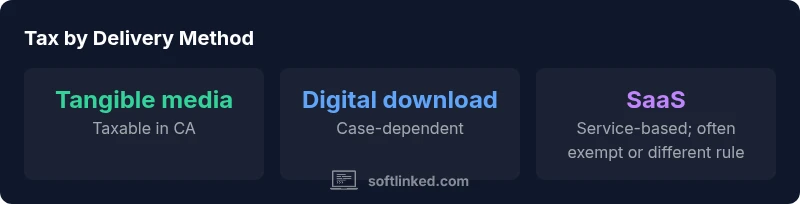

Delivery method matters: tangible media, digital download, and SaaS

The method by which customers receive software licenses is the primary determinant of tax treatment in California. Tangible media licenses (CDs, DVDs, USB drives) are taxed as tangible personal property. Digital download licenses can be treated as digital goods, and the taxability can depend on how the download is priced and delivered. SaaS and other cloud-based access arrangements are often treated as services rather than the sale of software, with tax outcomes varying by whether the service includes hosting, usage rights, or ongoing support. In practice, mixed licenses—where a license is bundled with media, updates, or installation services—require careful pricing separation to ensure the right tax treatment. If a contract states that the customer is purchasing a license for use and also receives ongoing maintenance, the taxability of each component may differ. Keeping line-item tax treatment transparent in invoices helps avoid ambiguity during audits.

Practical steps to determine taxability for your software license sale

- Map each transaction to delivery method: tangible media, digital download, or hosted access.

- Review contract language to determine whether the customer is buying a right to use software, access to a hosted environment, or both.

- Check CDTFA guidance for digital goods, software as a service, and licensing arrangements. CDTFA publications and e-guides are useful starting points.

- Separate pricing for software licenses, maintenance, and support on invoices to reflect potential tax differences.

- Consider how bundling with hardware or services affects taxability; if in doubt, perform a taxability assessment before invoicing.

- Maintain documentation of delivery method and jurisdiction in case of audits or audits by the CDTFA.

This approach reduces risk and supports accurate tax collection across state lines and multiple sales channels.

Common scenarios and edge cases

- A perpetual license delivered on physical media: typically taxed as tangible property in CA.

- A perpetual license with a download option but no hardware: often taxable as digital goods or potentially as a service depending on terms.

- A SaaS subscription: commonly treated as a service; taxability can vary by city or district within California; local rules may apply.

- Bundled licenses with hardware: tax treatment generally follows the tangible property rule for the bundle, necessitating allocation to components.

- International customers: use tax rules may differ, and cross-border transactions require careful VAT/GST considerations; consult local counsel.

These scenarios illustrate the importance of contract terms, delivery mode, and jurisdiction in modeling tax outcomes.

Recordkeeping and compliance considerations

- Keep copies of contracts, invoices, and delivery confirmations that specify the license type and delivery method.

- Track tax collected separately for each license type and avoid mixing digital goods with service charges on the same line item.

- Periodically review CDTFA updates and adopt changes promptly to stay compliant.

- When selling across multiple states, consider nexus rules and state-specific taxability rules for digital goods and software licenses.

Quality recordkeeping reduces risk and simplifies any potential audit processes and helps ensure that your tax treatment remains aligned with evolving state guidance.

Where to find official guidance and how SoftLinked helps

Official guidance comes from the California Department of Tax and Fee Administration (CDTFA) and related publications on digital goods, software as a service, and licensing. Because tax law changes frequently, it is wise to consult a tax professional and monitor CDTFA updates. SoftLinked helps aspiring software engineers and developers understand these fundamentals, offering clear explanations and practical checklists to navigate software licensing tax questions. By mapping license types to tax treatment, teams can price confidently, stay compliant, and reduce audit risk. The SoftLinked team recommends you stay informed and seek guidance when needed.

California tax treatment by software delivery method

| Delivery Method | Taxability (CA) | Notes |

|---|---|---|

| Tangible media license | Taxable when delivered on physical media | Bundling with hardware or services can affect taxability |

| Digital download license | Case-dependent; digital goods rules apply | Delivery method and pricing structure matter |

| SaaS / cloud access | Generally treated as a service | Taxability varies by service components and locality |

Your Questions Answered

Is a software license taxable in California if it's delivered as a download?

In California, downloadable software can be taxable as a digital good in some cases, depending on how it’s delivered and whether it’s bundled with tangible property.

Digital licenses can be taxable; check the delivery method and bundle details.

Are SaaS subscriptions taxed in California?

SaaS is typically treated as a service; taxability can vary by service components and locality within California.

SaaS tax rules depend on the service elements and where the customer is located.

Do exemptions apply to software licenses in California?

Exemptions may apply in some narrow cases (e.g., resale or government use). Most commercial licenses are taxed based on delivery method and contract terms.

Exemptions exist in specific scenarios; consult CDTFA guidance for details.

How should I invoice to reflect tax correctly?

Break out license, maintenance, and services on invoices when possible; clearly indicate delivery method and taxability per item.

Keep line-by-line tax details to simplify audits.

Where can I find official guidance on California software tax rules?

Check the CDTFA website and publications on digital goods, software services, and licensing for authoritative guidance.

CDTFA publications are the best starting point for official rules.

What about cross-border or international customers?

Cross-border sales may involve different tax rules (e.g., use tax, VAT/GST considerations). Consult a tax professional for multi-jurisdiction planning.

International sales add complexity; seek professional advice.

“Software licensing tax rules are nuanced and delivery-method dependent. Always verify with the CDTFA or a qualified tax professional.”

Top Takeaways

- Identify the delivery method first to determine taxability.

- Digital licenses and SaaS have nuanced CA rules; verify contract terms.

- Separate price components (license, maintenance, support) for accurate tax handling.

- Maintain detailed delivery and jurisdiction documentation for audits.

- Monitor CDTFA updates; tax rules for software licensing evolve.