Are Software Subscriptions Taxable in California? A Practical Guide

Explore whether California taxes software subscriptions, including SaaS and hosted services, with practical guidance, examples, and steps to stay compliant.

California tax treatment of software subscriptions (SaaS) is nuanced. In general, California taxes tangible property; however, digital goods and services, including SaaS, can be taxable depending on delivery method, bundled charges, and local jurisdictions. Businesses should review CDTFA guidance and consult tax professionals for specifics. This means the answer may vary by city and whether hosting, maintenance, or addons are billed separately.

How California taxes software: core rules for SaaS and digital goods

For businesses asking are software subscriptions taxable in california, the answer is nuanced. California's sales and use tax framework historically targets tangible personal property, but the rise of digital goods and software-as-a-service (SaaS) has created a complex landscape. In many SaaS arrangements, customers pay for ongoing access to hosted software, with updates, security, and data processing often bundled into one fee. The California Department of Tax and Fee Administration (CDTFA) offers guidance on digital goods and prewritten software delivered electronically, and SoftLinked's analysis in 2026 finds that some SaaS transactions are treated as taxable digital goods or services while others may be exempt depending on whether the charge is for access, hosting, or ancillary services. The practical takeaway is to classify the underlying transaction precisely: is the customer purchasing a license, a service, or a bundle that includes hosting or data processing? Invoicing clarity matters. If charges are separated, you can often distinguish taxable components from non-taxable ones. As markets evolve and providers roll out more cloud offerings, staying aligned with CDTFA guidance and local district tax tables is essential for accurate tax collection and reporting. The key is to audit subscription terms, confirm how charges are described on invoices, and monitor CDTFA updates for digital goods interpretations.

Delivery models and tax outcomes: SaaS vs licenses

Delivery model dramatically shapes tax outcomes in California. Pure download licenses (where software is delivered electronically) can be taxable as prewritten software in many circumstances, while true SaaS arrangements — where customers access software hosted remotely — may be taxed as a digital service or as software depending on how the sale is structured and what is bundled with it. Local district rules add another layer of complexity: some counties and cities levy additional district taxes that apply to software access, hosting, or ancillary services. Separate charges for hosting, maintenance, and support can be taxed differently from the base access fee. SoftLinked's approach in 2026 stresses the importance of prospectively analyzing each line item on an invoice: if you bill hosting separately, that component could trigger a different tax treatment than a simple access fee. Seek explicit guidance in CDTFA digital goods materials and verify the taxability status with the customer's location. In multi-jurisdiction scenarios, a single subscription may trigger multiple tax outcomes depending on where the service is used and where the customer resides.

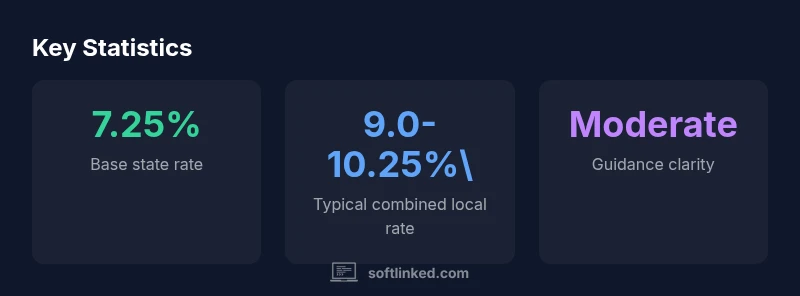

Local variability and sourcing: where tax is due

California uses destination-based sourcing for sales tax, which means the tax rate and applicability often depend on where the customer takes delivery or where the service is used. For software subscriptions, this frequently translates to the customer’s billing address or primary site of use. Localities within California may impose district taxes that apply to the sale of digital goods or services, adding to the base state rate. Because taxability can hinge on local rules and whether a charge is considered a taxable software sale, a non-taxable service, or a bundled offering, businesses operating across multiple jurisdictions must maintain precise records of customer locations and invoice details. SoftLinked analysis confirms that the taxability of software subscriptions is not uniform across the state; instead, it is shaped by delivery method, whether hosting is included, and how the vendor reports the charge to the CDTFA. When in doubt, consult CDTFA resources and verify the customer’s destination address to determine the correct rate and tax treatment.

Invoices, bundles, and bundled charges: how to bill

Billing practices strongly influence tax outcomes. If you present one lump-sum subscription price that includes hosting, updates, and support, the entire amount could be taxable in many California jurisdictions. If you separately state charges for hosting, data processing, and software access, each component might be taxed differently. The CDTFA guidance encourages transparent invoicing to prevent misclassification. For buyers, insist on itemized invoices showing which parts are taxable and which aren’t, to avoid disputes during audits. For sellers, it’s prudent to document the basis for taxability decisions, maintain copies of contracts that specify what is being delivered, and ensure your invoicing software consistently distinguishes taxable vs. non-taxable components. The interaction between bundled services and bundled charges is a common source of confusion; clarify which components are delivering software access versus services like hosting and maintenance.

Practical steps for compliance in California

To stay compliant when dealing with software subscriptions, start with a formal taxability determination for each product line. Register for California sales tax collection if you have nexus through customers in the state, employees, or servers; collect the applicable tax based on the customer’s location; and file periodic returns with CDTFA. Maintain a separate tax ledger for taxable and non-taxable charges, and ensure your contracts, quotes, and invoices clearly reflect the tax treatment. Periodically review CDTFA digital goods and prewritten software guidance, particularly if you add new subscription services or alter how you bundle offerings. For multi-state sellers, implement a robust multistate tax capability to handle destination-based rates and exemptions. Recordkeeping should include the delivery method, whether hosting is included, the exact scope of services, and any exemptions claimed by the customer. In short, the path to compliance demands clear categorization, precise invoicing, and staying updated with CDTFA’s evolving positions on digital goods and software subscriptions.

Quick-start checklist for SaaS providers and buyers

- Identify whether your product is delivered as SaaS (hosted) or as downloadable software.

- Confirm how charges are structured: is hosting or data processing bundled with access?

- Check the customer’s location and determine the appropriate local district rate.

- Issue itemized invoices that separately state taxable and non-taxable components.

- Align contracts with CDTFA guidance and keep records for audits.

- Reassess taxability when rules or product configurations change, especially with new cloud offerings.

- Work with a tax professional to review complex or multi-jurisdictional subscriptions.

- Monitor CDTFA updates and local district notices to adjust your pricing and filing processes accordingly.

Case studies and future outlook

As California continues to refine its treatment of digital goods and SaaS, many providers are re-evaluating their pricing, invoicing, and tax collection workflows. In practice, a subscription that includes hosting and data processing may be more likely to be taxed than a simple information-access service in some districts, while other localities may treat both as taxable digital goods. The SoftLinked team expects ongoing clarifications from CDTFA and potential updates to digital goods guidance as more businesses rely on cloud-based software. For buyers, the takeaway is to document use location, ensure accurate tax collection at the point of sale, and seek professional advice when entering multi-state contracts or when new services are introduced.

Taxability snapshot by delivery model

| Delivery Model | Taxability in CA | Notes |

|---|---|---|

| SaaS / cloud subscription | Depends on interpretation; often taxed as digital goods or service | Check CDTFA guidance and locality |

| On-premise license | Typically taxable when delivered as software; context matters | If delivered electronically, different rules may apply |

| Downloadable software (non-hosted) | Usually taxable as prewritten software in CA | Consider exemptions or bundled charges |

| Maintenance & support with subscription | Often taxable when bundled with software access | State guidance on bundling |

Your Questions Answered

Are software subscriptions taxable in California?

Yes, in many cases, software subscriptions (SaaS) are taxed as digital goods or services, depending on delivery and locality. Always verify with CDTFA.

SaaS tax rules in California depend on how the product is delivered and where the customer is located; check CDTFA guidance.

Is SaaS taxed as a service or as software?

California's treatment varies; some SaaS arrangements are taxed like software or digital goods, while others may be exempt as services. Review CDTFA guidance.

SaaS tax rules can treat it as software or a service depending on the specifics.

Do hosting or data processing fees get taxed with a subscription?

If hosting is part of the service, the bundled charge may be taxable; if the hosting is separate, the taxability may differ.

Bundled hosting can be taxable; separately stated hosting charges may not.

Do tax rates vary by city or county in California?

Yes. California uses destination-based sourcing and local district taxes, so rates differ by city and county.

Rates vary by location; always check the local rate.

Are there exemptions for nonprofits or educational institutions?

Certain exemptions may apply for nonprofit institutions, but they are limited and require proper documentation; always verify with CDTFA.

Nonprofits may have exemptions, but it's limited and often requires specific criteria.

“Tax rules for software subscriptions continue to evolve; businesses should plan for complexity, not risk.”

Top Takeaways

- Check CDTFA guidance first for taxability.

- SaaS tax outcomes depend on delivery and locality.

- Separate taxable charges from non-taxable services.

- Destination-based sourcing affects where tax is remitted.

- Maintain clear invoicing to separate taxable components.