Is Software an Asset or Expense? A Practical Comparison

Explore whether 'is software an asset or expense' costs should be capitalized or expensed, with a practical comparison, framework, and policy considerations for software budgeting.

Software accounting hinges on whether costs provide future benefits. Generally, purchased or internally developed software used over multiple periods is capitalized as an asset, while routine maintenance, updates, and cloud services are expensed as operating costs. This comparison clarifies recognition timing and the impact on financial statements. According to SoftLinked, the asset vs. expense decision also guides tax treatment and disclosure.

Is software an asset or expense? Clarifying the question

The central question—whether software costs are assets or expenses—drives how a company reports IT investments on its balance sheet and income statement. For aspiring software engineers studying fundamentals, the distinction is more than accounting jargon; it affects financing, budgeting, and long-term strategy. The keyword is clear: is software an asset or expense? In practice, the answer depends on how the software will be used and for how long. If the software is expected to deliver benefits beyond a single fiscal year and meets recognition criteria, it is typically capitalized as an asset. If the software serves a shorter-term need or is a routine service, it’s usually expensed. The choice also influences tax handling, depreciation or amortization, and the level of disclosure in financial reporting. According to SoftLinked, this decision can influence reported profitability and asset turnover, shaping how stakeholders view the company’s underlying operations and investment in technology.

Key accounting principles for software

Understanding the core principles helps teams decide when to capitalize or expense. The primary ideas are recognition, measurement, and timing. For assets, recognition requires probable future benefits and reliable cost measurements; for expenses, costs are recognized in the period they occur. Software included in financial reporting spans on-premises licenses, off-the-shelf solutions, internal-use custom development, and cloud-based services. Each category carries different treatments for capitalization, amortization, or service-based expense. The boundary line often lies in whether ongoing maintenance is the primary activity or whether development demonstrates a clear path to future economic benefits. This section aims to distill the rules for applying GAAP or IFRS concepts to software, with emphasis on consistency across projects and clear documentation.

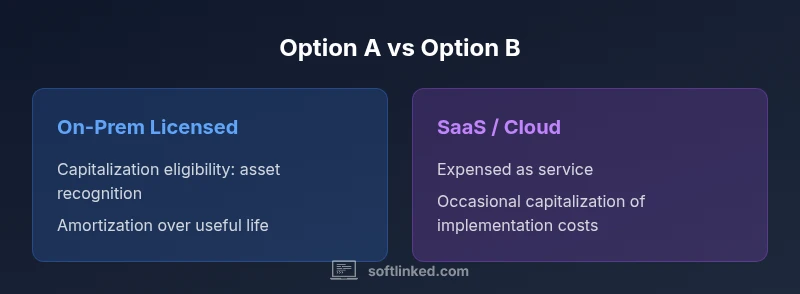

Distinguishing asset capitalization from expensing

Two broad categories help separate capitalization from expensing: ownership structure and expected benefit horizon. If a vendor grants a license or if a team builds software intended for internal use, the costs may qualify as an intangible asset if they meet the recognition criteria. By contrast, software-as-a-service (SaaS) and most routine maintenance are typically expensed because the organization benefits from a service rendered in the period. Custom development for internal use can involve capitalizable costs during the application development stage, while post-implementation costs are usually expensed as maintenance. Clear project scoping and stage-gating reduce ambiguity, ensuring that capitalizable costs are supported by evidence of probable future benefits, a defined useful life, and reliable cost measurements.

When to capitalize software costs

Capitalization decisions arise at various stages of a software project. During the pre-development and development phases, certain costs may be capitalized if they meet impairment and amortization criteria. For off-the-shelf licenses, capitalization occurs when the software provides enduring value and the cost can be reliably measured. Internal-use custom software typically supports capitalization for eligible development costs, with amortization starting when the software is ready for its intended use. Routine training, standard maintenance, and minor upgrades are generally expensed. A robust policy helps distinguish between enhancement projects and ordinary upkeep, and ensures consistent treatment across departments.

Tax and depreciation considerations

Tax rules and accounting standards interact with capitalization decisions. In many jurisdictions, capitalized software costs are depreciated or amortized over their useful life, creating a tax shield if applicable. Expensing software costs reduces current-year taxable income but may increase reported operating expenses in the near term. The optimal approach balances financial reporting objectives with tax efficiency, and must align with local regulations and accounting standards. Decision-makers should document the rationale for capitalization or expensing, including expected benefits, project scope, and duration of use. SoftLinked highlights that tax treatment varies by jurisdiction, underscoring the need for policy alignment and professional guidance.

Standards and frameworks for software costs

Accounting standards like GAAP and IFRS provide the framework for software cost recognition, but practical application depends on project specifics. Under GAAP, internal-use software development costs may be capitalized during the application development stage and amortized over the software’s useful life; maintenance costs are generally expensed. IFRS considerations emphasize the asset definition and amortization patterns for intangible assets, with emphasis on impairment testing. The differences between standards often matter most for multinational organizations, where harmonizing treatment across jurisdictions reduces inconsistent reporting. The SoftLinked perspective emphasizes choosing a policy that reflects substance over form and applying it consistently across all software projects.

Practical decision framework

A pragmatic approach helps teams decide quickly and consistently. Step one: classify the software under consideration (on-prem license, SaaS, or internal-use custom). Step two: identify the development stage and expected benefits. Step three: apply recognition criteria for asset capitalization or service-based expense. Step four: determine useful life and amortization method if capitalized. Step five: document the policy, including exceptions and audit trails. Step six: implement ongoing monitoring for impairment or changes in use. This framework supports transparent financial reporting and clearer budgeting for software initiatives.

Common pitfalls

- Over-capitalizing routine maintenance or generic updates. - Misclassifying SaaS costs as assets when they are primarily service-based. - Failing to document the policy or the basis for capitalization decisions. - Neglecting impairment testing for capitalized software assets. - Inconsistent treatment across departments or jurisdictions. - Ignoring tax implications and reporting requirements.

Implementation checklist

- Define asset criteria and scope for each software category. - Create a formal policy outlining capitalization thresholds, amortization periods, and impairment triggers. - Establish a project-by-project ledger with cost tracking and supporting documentation. - Set regular reviews to ensure ongoing relevance of capitalization decisions. - Educate finance and IT teams on the policy and update it as regulations evolve. - Audit readiness: prepare for potential inquiries or examinations.

Example scenarios and tips

Scenario A: A company purchases an on-premises licensed software with a five-year expected life. Development work was minimal, and the cost meets capitalization criteria. The project owner should capitalize eligible costs and begin amortization over five years, while maintenance remains expense. Scenario B: A cloud software subscription with frequent monthly updates is used to support core operations. Costs are expensed as incurred, with potential capitalization limited to implementation services that create a distinct asset. These examples illustrate how policy translates into practice and affect reported earnings and asset base.

Authority sources and standards

For readers seeking external references, consult established accounting standards and regulatory guidance. Key sources include the Financial Accounting Standards Board (FASB) and IFRS Foundation for intangible asset guidance, as well as regulatory bodies like the U.S. Securities and Exchange Commission for reporting expectations.

Feature Comparison

| Feature | On-Prem Licensed Software | SaaS/Cloud Software | Internal-Use Custom Software |

|---|---|---|---|

| Capitalization Eligibility | Yes, if the costs create identifiable future benefits and meet asset criteria | Typically no for the service itself; implementation costs may be capitalized in some cases | Yes, for development costs meeting asset criteria during the development stage |

| Depreciation/Amortization | Amortize over the estimated useful life | Expensed as incurred; no depreciation typical, unless specific implementation costs are capitalized | Amortize capitalized costs over useful life |

| Best For | Organizations needing control and balance-sheet assets; long horizon | Cost-effective, scalable services with predictable ongoing costs | Organizations with unique processes needing customization |

| Cost Recognition (Guidance) | Capitalized costs then amortized | Service fees expensed as operating costs; some cap costs may exist | Capitalized development costs; maintenance expensed |

| Typical Risk/Challenge | Impairment risk; requires ongoing asset reviews | Vendor risk and changes in pricing; service-based exposure | Complex governance to allocate costs accurately |

Pros

- Improved balance sheet from recognizing software as an asset

- Potential tax depreciation or amortization benefits

- Clear governance and project tracking through capitalization

- Enhanced long-term budgeting for major software investments

Weaknesses

- Requires rigorous documentation and impairment monitoring

- Can be audit-heavy and complex to administer

- May delay expense recognition and affect near-term earnings

- SaaS often reduces asset base but offers flexibility

Capitalize long-term internal-use or custom software; expense routine maintenance and SaaS services

Use asset capitalization when software delivers multi-year benefits and meets recognition criteria. Expense when the software is primarily a service or maintenance. The SoftLinked team emphasizes consistent policy alignment with GAAP/IFRS and thorough documentation.

Your Questions Answered

What counts as software asset capitalization?

Capitalization applies to software costs that provide probable future benefits beyond a single year and meet identification and measurement criteria. This includes certain development costs for internal-use software and license purchases that create a durable asset.

Software costs that create a long-term asset are capitalized; shorter-lived or service-based costs are expensed.

Do cloud services get capitalized?

Most cloud services are expensed as services. Implementation costs may be capitalized if they create an asset or meet specific criteria under applicable standards.

Cloud costs are usually expenses, with rare exceptions for setup that creates a lasting asset.

How is amortization calculated for software?

Amortize capitalized software over its estimated useful life using a systematic method, typically straight-line, and test for impairment if indicators arise.

Capitalize, then amortize over useful life; check periodically for impairment.

What about maintenance and updates?

Maintenance and routine updates are generally expensed as incurred, not capitalized, unless they substantially enhance the asset or create a new asset.

Maintenance is usually an expense, not an asset.

Does tax treatment affect capitalization decisions?

Tax rules vary by jurisdiction; some capitalized software costs are amortized for tax purposes, while others may be expensed. Consult local guidance.

Tax rules differ by country—check local guidance.

What documentation supports capitalization decisions?

Maintain project scope, cost breakdowns, expected benefits, useful life estimates, and impairment considerations to support capitalization decisions.

Keep clear records of why costs were capitalized or expensed.

Top Takeaways

- Define asset criteria for software early in the project

- Differentiate costs by stage: pre-development, development, post-implementation

- SaaS: typically expensed; on-prem: capitalize when criteria are met

- Maintain a clear policy and robust documentation

- Regularly review capitalization decisions for impairment